Introduction

Most farm families know they should have a succession plan. Most don't.

According to AgWeb's 2026 analysis, only 34% of growing farm operations have a formal succession plan — and among at-risk operations, that number drops to just 21%. Meanwhile, the average U.S. farm producer is now 58.1 years old, and approximately 44 million acres of U.S. cropland are projected to change hands by 2030.

That gap between awareness and action is closing fast.

When succession goes unplanned, the consequences extend well beyond paperwork. Farms face legal disputes, forced sales, family fractures, and the loss of something irreplaceable: a working land legacy that often spans generations. A good succession plan takes years to build properly. Starting late doesn't just create stress; it removes options.

This guide is built to help you close that gap. It covers what farm succession planning actually involves, the key components every plan needs, how to navigate family dynamics, asset transfer strategies, and the tax and legal considerations that determine whether your plan holds up.

Key Takeaways

- Only 34% of growing farm operations have a formal succession plan — most families wait too long to start

- A complete plan covers goals, successors, assets, legal documents, tax strategy, and family communication

- Farming and non-farming heirs need different treatment: splitting assets equally between them often forces a farm sale

- Inherited land gets a step-up in basis at death; gifted land carries over the donor's original cost basis

- The federal estate tax exemption rises to $15 million per individual in 2026, but state taxes vary widely

- Start planning at least 3–5 years before your intended transition; beginning 10+ years out gives the best outcomes

What Is Farm Succession Planning and Why Does It Matter?

Farm succession planning is the structured process of transferring ownership, management, and operations of a farm to the next generation — whether to a family member, trusted employee, or outside operator. It goes far beyond writing a will.

A complete succession plan addresses who takes over, when they take over, how assets transfer, how taxes are managed, and how the retiring owner will be financially supported.

It also tackles harder edge cases: What if the intended successor isn't ready? What if heirs disagree? What if no family member wants to farm?

Why Agriculture Is Different

Farms carry a kind of complexity that most other family businesses don't. A single property is simultaneously:

- A family home and personal identity

- A business generating income

- A livelihood for employees and neighboring families

- A community institution in rural areas

- An environmental asset tied to land health and water quality

An unplanned transition disrupts all of these at once. Operations stall during probate. Equipment sits idle. Tenants receive conflicting instructions. Heirs who never worked the land suddenly hold equal legal claim to it.

Why You Should Start 3–5 Years Out

That layered complexity is exactly why timing matters. A comprehensive farm succession plan takes 12–24 months to execute — and that estimate doesn't include the time needed to reach family agreement before planning begins. Most advisors recommend starting 3–5 years before the intended transition at minimum.

Waiting until retirement age creates a compressed timeline that eliminates many of the most effective strategies: gradual ownership transfer, mentorship of the successor, tax-efficient gifting programs, and entity restructuring. Starting early keeps all of those options on the table — and gives families room to reach agreement without financial pressure forcing the decision.

Key Components of a Farm Succession Plan

No two farm succession plans look identical, but every solid plan covers the same core elements.

1. Define the Owner's Goals

Before anything else, the retiring generation needs clarity on what they want. This includes:

- How much retirement income is needed, and from what sources

- Whether the farm should remain in the family or be sold

- Any charitable giving intentions

- What "a good legacy" actually means to them

These answers drive every subsequent decision. A retiring farmer who needs substantial income from the land sale has different options than one whose retirement is funded by outside assets.

2. Identify and Prepare the Successor

Identifying a successor early shapes the entire plan. This means evaluating both interest and capability — two things that don't always travel together. A child who loves the farm may lack the business skills to manage it. One who has the skills may not want the responsibility.

The successor's readiness assessment should happen years before the transition, creating time for mentorship, skill development, and gradual responsibility transfer.

3. Conduct a Full Financial Inventory

A succession plan built on incomplete financial information is a plan that will fail. This step involves:

- Inventorying all assets: land, equipment, livestock, non-farm investments

- Assessing outstanding debts and liabilities

- Analyzing cash flow to determine whether the farm can support the retiring owner's needs while remaining viable for the next generation

Financial review should also surface agronomic and operational realities. A farm that looks sound on a balance sheet may carry soil health problems, infrastructure deficits, or market access gaps that will quietly undermine the next generation.

Solutions in the Land's whole-system farm planning process works through 143 specific questions covering regional context, current conditions, opportunities, constraints, and revenue potential — giving families an operational foundation to build the transition on, not discover problems after it's done.

4. Build the Legal Documentation

Legal documents turn intentions into enforceable agreements. At minimum, a farm succession plan requires:

- A current will that reflects actual succession intentions

- Trusts (revocable or irrevocable) to manage asset transfer and avoid probate

- Buy-sell agreements governing how the farming heir can purchase the farm from the estate or other heirs

- Power of attorney and healthcare directives for unexpected incapacity

These documents require regular review. A will written when children were young needs updating when those children are adults with their own families and careers.

5. Assemble a Professional Team

Farm succession is too complex for any single advisor. An effective team typically includes:

- An estate attorney experienced in agricultural transfers

- A CPA with farm tax expertise

- A financial planner to model retirement income scenarios

- An insurance agent to evaluate life insurance strategies

- An agricultural consultant to assess operational viability

Each advisor covers a different dimension of the plan. In practice, the agronomic and land-use assessment is the piece most often added late or skipped entirely. Bringing in agricultural consulting early — before legal and financial structures are set — ensures the plan reflects what the land can actually support.

Identifying Your Successor and Navigating Family Dynamics

The Single-Heir Scenario

When one person is the clear successor, the path is more straightforward — but it still requires a formal will, a defined transition timeline, and a deliberate mentorship period. What feels settled in conversation is not legally binding until it's in writing — and a succession plan without documentation is just a wish.

The Multi-Heir Scenario

When multiple heirs exist, the complexity increases substantially. The single most important distinction to make early is between farming heirs (those who will actively operate the farm) and non-farming heirs (those who may inherit but won't work the land). Treating them identically is where most plans go wrong.

Three common approaches to multi-heir asset division:

- Separate farm and non-farm assets — farming heir receives farm assets; non-farming heirs receive equivalent non-farm assets (investments, life insurance, cash)

- Installment purchase — farming heir buys out non-farming heirs over time, keeping the farm intact and operational

- Equal land division — each heir receives a proportional share of land; this is the most common and most problematic option, as it often fragments the operation below viable scale

Land fragmentation is one of the most persistent problems in farm succession. Once divided, reassembling it is expensive and rarely achievable.

When No Family Successor Exists

This scenario is more common than most families expect. Options include:

- Identifying a trusted long-term employee as a successor operator

- Connecting with young farmer programs like the USDA Beginning Farmer and Rancher Development Program or land-matching services through American Farmland Trust's Farms for a New Generation initiative

- Bringing in a professional farm manager to operate while ownership transfers gradually

- Working with an agricultural consultant like Solutions in the Land to structure lease or partnership arrangements that keep the land productive during ownership transition

Family Communication Is Not Optional

Regardless of which scenario above applies to your farm, communication failures derail more succession plans than legal or financial ones. University of Wisconsin-Madison Extension identifies five primary tension points in farm succession:

- Finances

- Communication

- Inheritance

- Control

- Resistance to change

Communication problems underlie most of the others.

Structured family meetings with a defined agenda, clear roles, and documented outcomes produce better results than informal conversations. All parties need to understand the plan and their role in it before documents are signed, not after.

Transferring Farm Assets: Land, Equipment, and Livestock

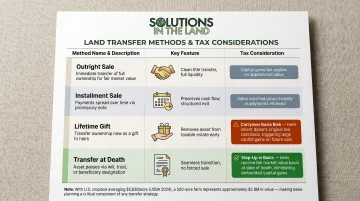

Land Transfer Options

| Method | Key Feature | Tax Consideration |

|---|---|---|

| Outright sale | Immediate cash, clean transfer | Capital gains on appreciation |

| Installment sale | Spreads gain over multiple years | Taxed as payments received (IRS Pub. 537) |

| Lifetime gift | Transfers control now | Carryover basis — recipient inherits your original cost basis |

| Transfer at death | Step-up in basis eliminates lifetime gains | Bypasses capital gains on prior appreciation |

The step-up in basis at death is one of the most significant tax advantages available in farm succession. When land is inherited, its cost basis resets to fair market value on the date of death — eliminating capital gains on all prior appreciation. By contrast, land gifted during the owner's lifetime carries over the original (often very low) cost basis, which can create a substantial tax liability when the recipient eventually sells.

With U.S. cropland averaging $5,830 per acre in 2025, the gap between original purchase price and current value can be enormous — making this distinction worth understanding before any transfer decision.

Equipment and Livestock Transfers

Equipment transfer options each carry different income tax and gift tax consequences:

- Outright sale — straightforward, but triggers immediate income recognition

- Installment sale — spreads tax exposure over multiple years

- Lease-to-successor — keeps cash flowing while the successor builds equity

- Gifting — transfers ownership without a sale, but gift tax rules apply

Work with a tax advisor before choosing a method. For livestock, common strategies include:

- Selling breeding stock in installments to spread taxable income

- Establishing joint ownership of offspring between transferor and successor

- Timing market livestock transfers to coincide with low feed inventory levels, which reduces the seller's taxable income in the transfer year

Assessing Land Health Before Transfer

Asset values on paper don't always reflect what's happening in the soil. Before any transfer is finalized, the farm's long-term agronomic health deserves a hard look.

A successor inheriting degraded soils, poor water management infrastructure, or declining productivity is taking on a diminishing asset — regardless of what the balance sheet shows. Regenerative agriculture consulting can identify current conditions and map improvement pathways that strengthen both land value and productivity ahead of the transition. Solutions in the Land works with landowners at exactly this stage, helping ensure what gets transferred is an asset that performs.

Tax, Legal, and Estate Planning Considerations

Federal Estate Tax

The federal estate and gift tax exemption is $15 million per individual starting January 1, 2026, under the One Big Beautiful Bill Act — up from $13.99 million in 2025. Married couples can effectively double this through portability elections, reaching $30 million combined. The federal tax rate on amounts above the exemption remains 40%.

For many farm families, the federal exemption provides meaningful protection. But state-level estate and inheritance taxes are a different story — with exemption thresholds as low as $4 million in Illinois and inheritance taxes starting above $1,000 in Kentucky. Approximately 12–13 states plus Washington D.C. impose estate taxes, and 6 states impose inheritance taxes.

IRC Section 2032A offers an additional tool: qualifying farmland can be valued at its actual agricultural use value rather than highest-and-best-use (development) value. This can substantially reduce estate tax liability for farms near urban or suburban areas where development pressure inflates market value.

Annual Gifting Strategy

The IRS annual gift tax exclusion is $19,000 per recipient for both 2025 and 2026. Married couples can gift-split, effectively transferring $38,000 per recipient per year without touching the lifetime exemption. Used consistently over many years, annual gifting can meaningfully reduce the taxable estate.

Life Insurance as an Equalization Tool

Gifting reduces the taxable estate, but it doesn't address a separate challenge: what happens when one heir farms and others don't. Life insurance is often the most practical answer. A permanent life insurance policy — specifically a "second-to-die" policy — pays out after both parents have passed. That tax-free death benefit goes to off-farm heirs, while the farming heir inherits the physical assets.

When structured as an Irrevocable Life Insurance Trust (ILIT), the policy proceeds sit outside the taxable estate entirely, providing liquidity for estate taxes without adding to the estate's value.

Legal Structures

Three structures appear most often in farm succession:

- LLCs — enable gradual ownership transfer through membership interests while keeping management control with designated managers

- Family limited partnerships — offer similar ownership flexibility, often with valuation discounts that reduce the taxable gift value

- Revocable trusts — avoid probate and remain easy to modify during your lifetime

- Irrevocable trusts — remove assets from the taxable estate entirely, though changes are difficult once established

Each has trade-offs. Work with a qualified estate attorney before establishing any of them.

Common Mistakes to Avoid in Farm Succession Planning

Waiting too long to start. Poor health, unexpected death, or a family crisis can force rushed decisions under the worst possible conditions. Plans made under pressure tend to be legally fragile, financially suboptimal, and emotionally damaging. The families who fare best started years before any transition was imminent.

Confusing equal with equitable. Dividing the farm equally among all heirs sounds fair. In practice, it often results in fragmented land parcels below viable operating scale, with none of the heirs able to farm profitably. An equitable plan assigns assets based on roles and actual needs — the farming heir gets the farm, non-farming heirs receive equivalent value through other means.

Avoiding the hard conversations. Silence about finances and future intentions is one of the leading causes of conflict in farm transitions. When heirs discover the plan for the first time after a parent's death, disputes are almost inevitable. Proactive, structured family meetings — where everyone understands the reasoning behind the plan — create alignment rather than resentment.

Failing to update documents. A plan written 15 years ago reflects a 15-year-old reality. Tax laws shift, heirs' circumstances evolve, and farm values can change dramatically within a decade. Plan for regular reviews — ideally every three to five years, or whenever a major life event occurs — to keep documents legally sound and aligned with current realities.

A review should cover at minimum:

- Estate and ownership documents (wills, trusts, deeds)

- Buy-sell agreements and lease terms

- Tax elections and entity structures

- Changes in heir circumstances (marriage, divorce, debt)

Frequently Asked Questions

What is a farm succession plan?

A farm succession plan is a documented strategy for transferring ownership, management, and operations of a farm to the next generation. It covers legal, financial, and operational considerations — wills, trusts, tax planning, successor preparation, and family communication — to ensure a smooth, intentional transition.

What are the key components of a farm succession plan?

The core elements include: goal-setting for the retiring owner, successor identification and mentorship, a full asset and debt inventory, legal documentation (wills, trusts, buy-sell agreements), a retirement income plan, and a structured family communication strategy.

What tax and estate issues should be considered in farm succession planning?

Key tax issues to address:

- Capital gains tax on land sales and the step-up in basis at death

- Annual gift tax exclusions ($19,000 per recipient in 2025–2026)

- Federal estate tax exemption ($15 million per individual in 2026)

- State-level estate or inheritance taxes

Consult a CPA and estate attorney — farmland values make professional guidance critical.

How do capital gains and inheritance taxes affect inherited farmland?

Inherited farmland receives a step-up in cost basis to fair market value at the owner's death, eliminating capital gains on prior appreciation — so get a professional appraisal at that time to document it. Gifted land retains the donor's original basis, which can trigger significant capital gains tax if the recipient later sells.

What happens to a farm when the owner dies without a succession plan?

Without a plan, the farm passes through probate under state intestate succession laws — a process lasting months to over a year and costing 3%–10% of the estate's value. If heirs can't agree on ownership or management, a forced sale is a real risk. Farm operations often stall throughout.

What are common mistakes to avoid in farm succession planning?

The most common: starting too late, treating equal distribution as the same as equitable distribution, avoiding difficult family conversations, and failing to update legal documents after major life or financial changes. Each of these mistakes is avoidable with early, structured planning.